Workers' Compensation insurance (also called Workers' Comp coverage and Workers' Comp insurance) provides financial protection for employees who are injured, become ill, or die on the job. In doing so, it also protects businesses and negates the need for lengthy and often stressful financial battles.

What is Workers' Compensation? Why was Workers' Compensation insurance created? How does Workers' Comp work? What are the typical Workers' Compensation benefits? How do you get coverage? What does it cost? You'll be able to find out everything you need to know about Workers' Compensation insurance for small businesses here in our detailed guide.

Who benefits from this guide to Workers’ Compensation insurance?

Understanding what workers’ compensation insurance is and how it works is crucial for three primary groups:

- Small business owners. This guide provides vital insights on workers’ comp, including how to get affordable coverage. It also explains that having coverage typically is necessary to comply with state regulations and avoid fines, penalties, and other potential pitfalls. Plus, it’s a helpful reminder to consider risk management initiatives that reduce the likelihood of workplace injuries.

- Human resources professionals. It’s crucial that you have an in-depth understanding of workers’ compensation insurance so you can assist employees who’ve been injured as they file a claim, advocate for workplace safety initiatives, develop educational resources for workers, and help management understand your workers’ comp policy.

- Frontline employees. This guide explains your rights following an on-the-job injury, what’s involved in filing a claim, and your role in ensuring that the workplace is as safe as possible.

What types of businesses are required to have Workers’ Compensation insurance?

Employees are protected financially by Workers' Compensation, meaning it protects those who are injured, get sick, or die as the result of a work-related incident. Workers' Compensation benefits include coverage for medical costs, legal fees, and lost employee wages. It can also pay what’s called a death benefit to a worker's family if an employee dies as a result of an on-the-job accident.

Workers' Compensation insurance requirements vary by state and it's important to make sure you check out all the legal requirements of each place before you purchase Workers' Comp insurance. However, nearly every business that has employees—full-time, part-time, or seasonal—is required to carry Workers' Comp coverage. Failure to do so can often result in costly claims if an employee is injured on the job.

There are few exceptions to this rule. Consequently, if your business employs anyone, you should assume that you’re required to have a Workers' Comp policy unless you receive information from the Workers' Comp authority in your state explicitly stating that you don't have to have a policy. (You can also learn more about insurance requirements for your state on our website.)

You should also be aware that some states require Workers' Comp insurance for construction industry sole proprietors or those who pay subcontractors.

The Origins of Workers' Compensation Insurance

What is Workers' Compensation and how did it come into being? The U.S. Workers' Compensation insurance system was created in the early 1900s and modeled after principles already in place in Europe.

Before this system's development, employees injured at work had the right to sue employers for the cost of their medical care, lost wages, and other costs. However, to receive a Workers' Comp settlement, they had to prove that the company's negligence was the cause of their injury, and that was no easy task.

Typically, it required a long, expensive court battle. And because employers generally had greater resources for fighting this battle, they had an advantage.

Workers’ Compensation Insurance and the Industrial Revolution

As the Industrial Revolution gained momentum and greater numbers of employees were working with and around machinery, the risk of injury or death at work increased. As it did, two forces were catalysts for the Workers' Compensation insurance system. One was the voice of employees and their families, who faced financial ruin if the main breadwinner was severely injured or killed in a work accident.

The second was the recognition by employers that a large number of lawsuits from injured employees could hurt their profits. Companies also began to compare the costs associated with having to hire and train new employees as compared to the cost of supporting well-trained workers until they could get back their jobs. They found that keeping good employees made financial sense.

Ultimately, the Workers' Comp coverage system and supporting laws were developed, with all stakeholders finding it to be a more collaborative and humane way to address worker injuries, illnesses, and fatalities.

What benefits does Workers’ Comp coverage offer?

Workers’ Comp insurance is an important employee benefit. It provides four main types of financial protection:

- Medical coverage. This includes hospital care, doctor visits, nursing care, medication, medical tests, physical therapy, and what's called durable medical equipment—items like wheelchairs and crutches.

- Disability benefits. This wage replacement is paid directly to the employee for income lost as a result of the incident. There are different categories of disability: temporary total, temporary partial, permanent total, and permanent partial disability.

- Vocational rehabilitation assistance. Most states require that employers provide some form of vocational rehabilitation for workers who can't return to their previous job due to their injuries.

- Death benefits.If a worker dies as a result of an on-the-job injury, their spouse and minor children receive a death benefit that includes coverage for funeral costs.

The goal of these benefits is to ensure that employees and their families aren't left with a large financial burden following an on-the-job injury.

It's important to note that Workers' Compensation insurance policies don't provide benefits in all instances. For example, if the person who files the claim injured themself intentionally or suffered an injury as a result of intoxication or substance abuse, their claim may be denied. And those are just a few examples of exclusions. Employees and employers need to understand what's covered by Workers' Compensation insurance and what's not covered.

How to Purchase Workers’ Compensation Insurance

biBerk makes buying Workers' Comp coverage easy and we offer the best workers' comp insurance for small businesses. A good place to start is getting an instant online Workers' Compensation insurance quote. The cost of a Workers' Comp policy is based on several factors, most notably your company's gross annual payroll. The higher your payroll is, the higher your premium will be.

Specifically, the cost is calculated as a rate (which is determined based on the type of work your company performs) that is then multiplied by your payroll. What's called an experience modification or ExMod is also applied if your company has one. It's a figure used to compare your loss history to the average in your industry.

Once you have your Workers' Compensation insurance quote and decide to make your purchase, you can do that online, too. Insurance can be purchased in a matter of minutes, with coverage active soon after the transaction is completed—within a day or two in most cases.

Business owners should be aware that at the end of a Workers' Comp insurance policy period, the insurer performs what's called an insurance audit (see below) to ensure that the right amount was paid for the coverage, taking into account any changes that occurred during the policy period, such as increasing or decreasing employee payroll.

What’s a Workers’ Comp Exemption?

Particularly for a small business, workers’ comp insurance is vital. However, there are certain people you may not want to cover with your policy.

If that’s the case, you can request what’s called a workers’ compensation insurance exemption. If the request is granted, you aren’t required to provide insurance for the person or people covered by the exemption.

A workers’ comp exemption may be granted in some states for people like:

- Self-employed individuals

- Independent contractors

- Business owners and officers

- Domestic workers

- Farm workers

- Government workers

- Railroad employees

- Longshoremen and other maritime workers

- Volunteers

Each state has its own workers’ compensation requirements, so you must understand the regulations that apply to your business.

It’s also important to be aware of the risks associated with not covering someone, especially yourself. If you’re a sole proprietor, are granted a workers’ comp exemption, and decide not to get workers’ comp insurance, you may be faced with paying your medical costs out of pocket if you suffer a work-related injury and your health insurance doesn’t cover them.

Workers’ comp for business owners can be a crucial part of a company’s overall insurance protection.

What’s a Workers’ Comp insurance audit?

In a Workers' Comp insurance audit, an auditor reviews your records to determine your total payroll for the policy period. The pay for some employees—like owners and officers—may be excluded from a company's total payroll if the business owners/officers elected to be excluded properly at or before the inception of the policy. If owners/officers are included, their payroll may be adjusted to meet state-required annual minimums/maximums per owner/officer.

A Workers' Comp audit doesn't change the rate in your original policy. Rather, it calculates the actual payroll amount to which the rate is applied. The auditor also checks to see if all independent contractors/subcontractors you used during the policy period had their own coverage in place. If not, you may be charged an additional premium for the independent contractors/subcontractors.

How does a Workers’ Comp insurance audit work?

A Workers' Comp audit is a very straightforward process in which you provide requested information to the auditor. However, you can further streamline the process by finding certain information in advance, including:

- A detailed business description. The type of work you do affects the Workers' Compensation classification codes that are used for your business and the associated rates. Work involving a higher degree of risk has a higher rate than less-hazardous work. The auditor will need to develop an in-depth understanding of your operations.

- Employee records. These records should include a detailed description of each employee’s duties and the number of hours worked during the policy period.

- Payroll records. Documents like a payroll journal, federal tax reports, individual earnings records, and overtime payroll records are needed.

- Payments. The auditor will need details on payments to independent contractors and subcontractors, as well as casual labor payments and materials purchases.

- Certificates of Insurance. The auditor will want to see any Certificates of Insurance provided to you by independent contractors or subcontractors you used during the policy period.

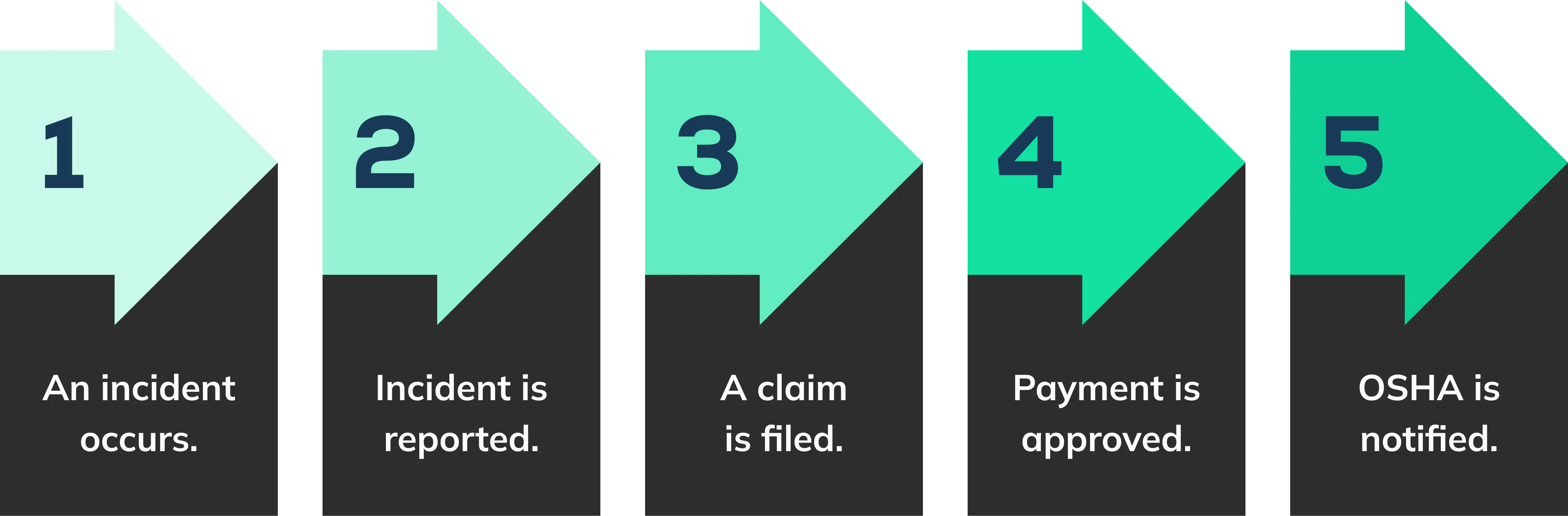

How does a Workers’ Comp insurance claim work?

As with many elements of Workers' Compensation insurance, the claims process varies from state to state, and you should always learn about the rules and regulations where you live. However, in general, it flows as follows:

- An incident occurs. An incident occurs and an employee suffers an on-the-job injury.

- The incident is reported. The employee reports the injury to their supervisor and/or the company's human resources (HR) department. This must be done within a certain time frame or the employee may forfeit their benefits under the policy.

- A claim is filed. The company or injured worker files a claim with the insurance company.

- Payment is approved. The insurance company evaluates the claim and determines the payments based on the statutory Workers' Comp regulations for the state in which the incident occurred.

- OSHA is notified. The company must also report the incident to the Occupational Safety and Health Administration (OSHA) in 8-24 hours, depending on the severity of the injury.

How much does Workers’ Compensation insurance pay for wage replacement?

The amount that a Workers' Compensation insurance policy pays for wage replacement if an employee can't work due to an on-the-job injury is based on several factors, including:

- The employee's pay rate

- The type of injury or illness

- Whether they suffered a temporary or permanent injury

- In the case of a disability, whether they are partially or totally disabled

- The Workers' Comp laws in their state

In addition, hourly wage indemnifications are subject to state set minimums and maximums.

Frequently Asked Questions About Workers' Comp Insurance

How does Workers' Comp work and what does Workers' Comp cover?

Having Workers' Compensation insurance in place before anyone gets hurt is important and required in most instances. It's also crucial to answer employee questions about the policy, like, “What does Workers' Comp cover?”

Then, if someone does get injured at work, the most important thing is to address the injury promptly and correctly and ensure that no other employees are at risk. Once you've dealt with the crisis, it's important to gather all the available information about the incident. This includes talking with witnesses, taking photos of the injury site, obtaining security camera footage, etc.

How do I know if my workers’ comp claim is approved?

As soon as possible, work with the employee to file a workers’ comp coverage claim. Once you’ve done that, it’s important to stay in contact with the employee as the claims process progresses. Open lines of communication are essential for getting the injured employee the care and compensation they need. Injured workers may find out if their claim has been approved in as little as 15 days after the claim has been submitted and assessed.

How much does workers’ comp cost?

It’s important to be aware of how much workers’ comp can cost. An individual’s injury is given a rating based on what’s called an Impairment Rating Evaluation (IRE). Independent professionals use this rating scale to quantify an employee’s level of impairment. The rating they assign helps the worker, their employee, and the workers’ comp insurance provider stay on the same page regarding ongoing compensation for the employee’s injury.

For example, an employee’s rating may reflect that they have a temporary partial disability and will be able to return to work at some point. In that scenario, the person’s workers’ comp benefits will be temporary. If a rating indicates that a worker has a permanent total disability, they may receive permanent benefits.

Each state has its own impairment guidelines. Consequently, you shouldn’t assume that the way a particular type of injury was handled and compensated in one state will be the same in another state. It’s crucial to be aware of the rules and regulations of the state you live in, and keep abreast of any changes to legislation. Failure to do so could be costly for both you and your employees.

What is worker classification and why does it matter?

For the purposes of workers’ compensation insurance, people who perform work for you can be classified as employees or independent contractors/subcontractors. This distinction is important because you’re required to provide workers’ comp coverage for employees in virtually all instances, but that’s not the case with independent contractors/subcontractors.

Independent contractors/subcontractors must have workers’ compensation coverage, but you can require that they have their own workers’ comp policy as a condition of you hiring them. Then you must obtain proof that they have coverage in the form of a Certificate of Insurance.

What happens if I misclassify workers?

If you misclassify an independent contractor as an employee or vice versa, that mistake can be costly. It will almost certainly affect your insurance cost when the workers’ compensation insurer conducts your workers’ comp audit.

In some cases, it may mean that you have to pay an additional premium at the end of your policy period. Therefore, it’s important to be sure that you and your workers are clear on what type of business relationship you have.

Do I need workers’ compensation insurance if I’m self-employed?

The rules regarding workers’ comp insurance and self-employed people vary by state, so you must check the laws where you live. However, having coverage for yourself may be helpful for a few reasons.

One is that your health insurance may not cover the cost of injuries that occur while you’re working but workers’ comp coverage typically will. Another is that a workers’ comp policy may pay for some of your lost wages while you recover from an injury.

In addition, the companies you do work for may require that you have workers’ compensation insurance coverage. Consequently, getting a workers’ comp policy generally is a wise business decision.

Does workers’ compensation insurance cover employee lawsuits?

Workers’ compensation insurance includes employer’s liability coverage. That means it protects the business if an employee sues for certain reasons outside of workers' compensation claims.

For example, what’s called employer's liability may apply if a non-employee is injured indirectly by a workers' comp insurance claim, such as a spouse who is taking care of a temporarily disabled worker and is injured in the process, or if a spouse sues for loss of consortium.

However, this isn’t blanket coverage for any type of lawsuit. It’s important to talk with your workers’ comp insurance provider about the parameters of the protection offered.

Does health insurance cover work-related injuries?

Health insurance policies vary. However, many won’t pay the medical bills resulting from an on-the-job injury. That’s why it’s so important for employers to have workers’ compensation insurance—not to mention that it’s the law in most cases.

Workers’ comp coverage gives workers and employers the confidence of knowing that the costs of work-related injuries, illnesses, and fatalities can be addressed by the policy. With coverage in place, no one will end up with a large financial burden as a result of an incident.

When it comes to getting the different types of small business insurance your company needs, workers’ compensation coverage should be at the top of your list!

Is workers’ comp taxable?

Employers and employees should talk with their respective tax advisors about how workers’ compensation insurance benefits affect tax liability.

Talk to biBerk today for the best Workers’ Comp insurance for small business.

Whatever your workers' compensation insurance requirements are, biBerk can help you make the right decision for your small business.

We're part of the Berkshire Hathaway Insurance Group and have been helping companies get the financial protection they need for over 75 years. You can trust us to help you with all your business insurance requirements.

Our friendly licensed insurance experts are happy to take your calls and answer any questions you may have. We're also here for you after you purchase your policies!

About the Author

Adam Pevarnik

Chief Underwriting Officer

Adam Pevarnik leads underwriting strategy and product development for biBerk, ensuring pricing and guidelines align with the company’s mission to serve small businesses effectively. An actuary by training with Berkshire Hathaway experience across underwriting, product, and reinsurance roles, he brings analytical rigor to content on risk selection and portfolio performance. Adam’s articles offer actionable insights into balancing underwriting discipline with insurtech innovations.